- Organic Agriculture as a Long-Term Strategy

- Organic Market Report for Texas Organic Farmers

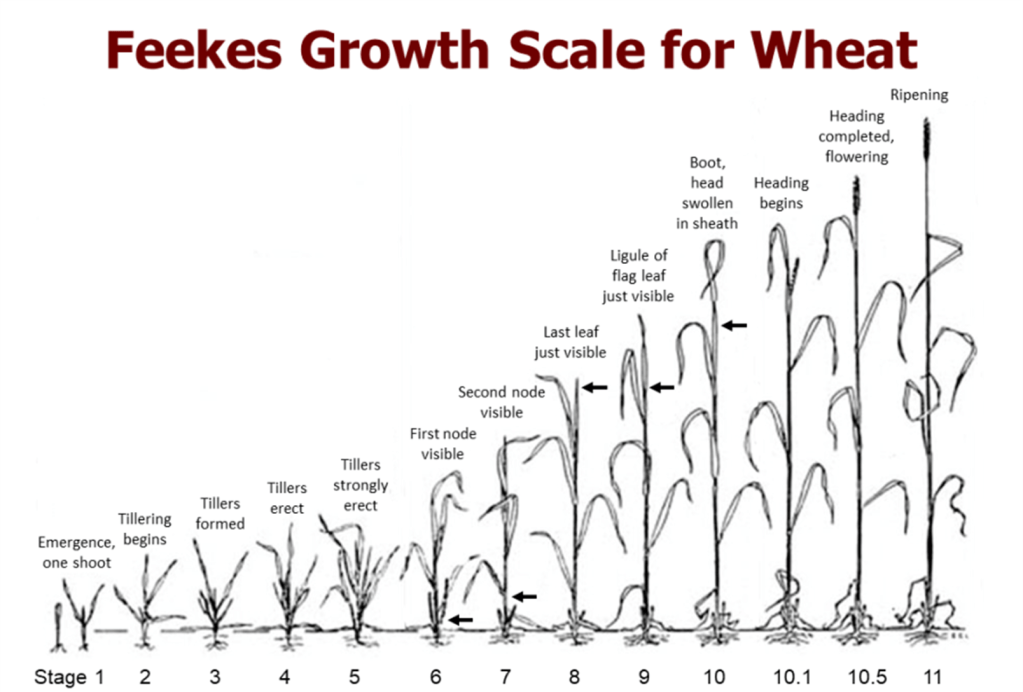

- Organic Wheat

- Organic Corn

- Organic Dairy

- Organic Soybeans

- Organic Integrity and Import Oversight Expand Under USDA SOE Rule

- Sources and Market References

Organic Agriculture as a Long-Term Strategy

Organic agriculture is increasingly revealing itself as more than simply a production system built around prohibited substances. Over the long term, it may be better understood as a biological and economic strategy centered on trust, resilience, traceability, and system function. While conventional agriculture often optimized around maximum efficiency, scale, and external inputs, organic agriculture has gradually emphasized relationships between soil biology, nutrient cycling, biodiversity, food quality, and consumer confidence. The USDA National Organic Program helped create a framework where consumers can trust production methods they cannot personally observe, making organic agriculture as much a transparency system as a farming system. At the same time, many long-term organic farmers increasingly report that mature organic systems (greater than 5-7 years) often become less dependent on purchased inputs as soil health, rotations, and biological regulation improve over time.

I hear often from farmers, bakers, dairy processors, and food manufacturers who frequently report differences in flavor, functionality, storage, processing quality, and handling characteristics that go beyond simple yield measurements. Meanwhile, rising transportation costs, supply-chain complexity, and consumer interest in traceability may and do, increasingly favor organic systems. Also, we are seeing technologies such as digital traceability, AI-driven compliance systems, and integrated recordkeeping beginning to reduce some of the traditional burdens associated with organic certification.

These broader trends are also becoming increasingly visible within organic grain and dairy markets themselves, where pricing is often shaped less by simple commodity production and more by quality, traceability, transportation, end use, and long-term supply relationships. Current (Jan. to May 2026) USDA AMS reports and organic market activity continue to show that organic agriculture operates through highly differentiated markets where buyer confidence, dependable supply, and product identity can significantly influence value.

Organic Market Report for Texas Organic Farmers

Organic markets continue to show strong differentiation by quality, delivery structure, end use, and contract type rather than functioning as simple commodity markets. Across grains and dairy, USDA AMS reports continue to show active forward contracting, regional price variation, and premiums tied to quality, storage, transportation, and dependable supply relationships. While organic market reporting remains in “short supply” in some Southern regions, including Texas, the overall market signals suggest that buyers continue working to secure reliable supplies of organic feed grains, food-grade products, and dairy inputs well ahead of delivery.

Organic Wheat

Organic wheat prices remain highly differentiated by class, protein, buyer type, delivery terms, and contract structure. In recent AMS reports, Soft Red Winter values often fall in the high single digits to low teens, while Hard Red Spring commands a stronger premium, with some flour-mill forward contracts reaching $20/bu. The main takeaway is that organic wheat is priced less as a generic commodity and more as a set of niche markets defined by end use, quality, freight terms, and whether the transaction is spot, bid, or forward contracted.

For Texas organic wheat farmers, this means harvest is also a marketing decision. Growers who can protect test weight, maintain protein, and keep grain clean and dry are in the best position to capture milling premiums, while those selling quickly into generic feed or elevator channels may leave money on the table. Before cutting, it is worth comparing buyers, delivery terms, and contract options, because in this market the details can matter as much as the wheat itself.

Organic Corn

Organic corn markets continue to show relatively strong and stable pricing compared to many other organic commodities, with much of the AMS-reported activity clustering around the mid-$10 per bushel range (but I see it steadily increasing). Prices still vary by location, contract structure, and whether the grain is old crop or new crop, but the overall pattern suggests a market supported by steady feed demand, active forward contracting, and ongoing regional supply shortages. Unlike organic wheat, where protein and milling quality create wider price separation, organic corn remains heavily influenced by livestock feed demand, freight costs, and regional availability.

For Texas organic corn growers, the message is to stay flexible and market carefully checking regularly on prices. Producers who can store grain, preserve quality, and deliver into specialty feed, dairy, poultry, or food-grade channels may be able to capture better returns than those forced to sell at harvest. Transportation costs and local buyer demand can make a meaningful difference, particularly in regions where organic feed supplies remain limited. Forward contracts (some but not all!) also remain important because they help secure long-term supply relationships and reduce risk in a market that continues rewarding dependable volume and consistent quality.

Organic Dairy

The USDA Organic Dairy Market News Report for May 4–15 provides a snapshot of current organic dairy market conditions rather than a policy or technical standards document. The report shows that organic milk demand remained strong during spring 2026, with U.S. sales of total organic milk products up 5.6 percent for March and organic whole milk sales also showing strong year-over-year growth. Retail organic dairy products, especially milk and yogurt, continue maintaining noticeable price premiums, reflecting continued consumer demand for organic dairy products and broader interest in food products associated with transparency, animal welfare, and ingredient sourcing.

The report also demonstrates how closely the organic dairy sector remains tied to feed markets and broader supply conditions. Organic grain and feed markets remain active, with some forward contracts extending into 2027, indicating that buyers continue working to secure future supply. For producers, the overall signal is that organic dairy demand and premium pricing remain solid, but feed costs, export movement, and retail advertising trends continue shaping a competitive market that remains sensitive to supply and input conditions.

Organic Soybeans

I know we don’t produce many organic soybeans, but they do indicate some import protein trends. Organic soybean markets continue showing some of the strongest structural support among major organic grain commodities, with pricing being driven largely by protein demand, livestock feed markets, and food-grade specialty channels. Unlike organic wheat, where class and milling quality create major price separation, soybean values appear more closely tied to dependable supply, identity preservation, and end use. AMS-reported activity suggests that forward contracting remains active, indicating that buyers continue working to secure long-term supply in a market where domestic production remains limited and imported soybeans still influence overall availability and pricing.

For Texas organic producers, soybeans provide an important lesson even where acreage remains limited. Organic soybean markets demonstrate how protein quality, cleanliness, storage, and buyer relationships increasingly shape value in organic agriculture. Food-grade and identity-preserved soybeans can carry significant premiums over generic feed channels, reinforcing the idea that organic crops are often marketed less as bulk commodities and more as differentiated products tied to specific supply chains. The continued influence of imported soybeans also highlights the importance of dependable domestic production capable of meeting both feed and food-grade demand.

As Texas organic markets continue developing, similar trends may increasingly influence corn, sorghum, wheat, peanuts, and other crops where end use, traceability, and dependable supply relationships become more important than simple yield alone.

Organic Integrity and Import Oversight Expand Under USDA SOE Rule

The USDA National Organic Program continues expanding oversight of imported organic products through the Strengthening Organic Enforcement (SOE) rule. New Organic Insider reports highlight how USDA is now using import certificate data, shipment tracking, and compliance analytics to identify irregular trade patterns and investigate potential fraud before products reach the marketplace. Several recent investigations involved imported organic products lacking valid import certificates, while another case involving raspberries from Mexico demonstrated how residue testing and traceability systems prevented contaminated products from entering U.S. commerce. The increased emphasis on farm-to-market traceability reflects USDA’s growing focus on maintaining consumer confidence and strengthening enforcement throughout global organic supply chains.

The newly released 2025 organic import data also provide a revealing picture of the modern organic marketplace. Total U.S. organic imports approached $12 billion in 2025 (total organic sales in the US are $76 billion), with Mexico representing more than 20% of total import value. Organic beef, coffee, bananas, blueberries, avocados, olive oil, and processed soybean products ranked among the largest import categories. The data reinforce that organic agriculture has become deeply connected to international supply chains and value-added food manufacturing systems rather than operating solely as a domestic farm commodity market.

For U.S. organic producers, these trends highlight both continued strong consumer demand for organic products and the increasing importance of traceability, market relationships, and maintaining trust in the organic label. For Texas organic farmers specifically, future competitiveness may depend less on maximizing volume alone and more on building dependable supply relationships, preserving quality, improving traceability, and positioning farms within regional food systems that value identity preservation, biological function, and long-term resilience.

Sources and Market References

This market analysis and commentary were developed using information from the following USDA and industry reports:

- USDA AMS National Organic Feed Grain and Feedstuffs Report, January 1, 2026 – April 27, 2026

- USDA National Organic Program 2025 Organic Imports Report based on Organic Import Certificates

- USDA AMS Organic Insider Report, May 27, 2026

Additional market interpretation and analysis were developed through ongoing observations of organic grain, dairy, and specialty crop markets relevant to Texas organic producers.